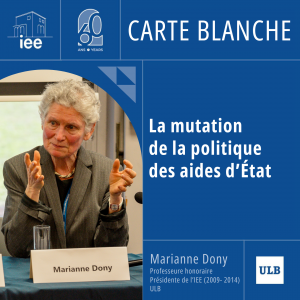

'60 years in 6000 characters' - "La mutation de la politique des aides d’État" by Marianne Dony

The series of cartes blanches, published to mark the sixtieth anniversary of the IEE-ULB, continues with an article by Marianne Dony.

Read More

The series of cartes blanches, published to mark the sixtieth anniversary of the IEE-ULB, continues with an article by Marianne Dony.

Read More

The series of cartes blanches, published to mark the sixtieth anniversary of the IEE-ULB, continues with an article by Jean-François Bellis.

Read More

The series of cartes blanches, published to mark the sixtieth anniversary of the IEE-ULB, continues with an article by Anna Zech.

Read More

The IEE-ULB is delighted to welcome Soso Makaradze from the University of Salzburg. His research activities will focus on EU integration, democratic backsliding and public opinion.

Read More

The series of cartes blanches, published to mark the sixtieth anniversary of the IEE-ULB, continues with an article by Giulia La Torre.

Read More

The series of cartes blanches, published to mark the sixtieth anniversary of the IEE-ULB, continues with an article by Ilaria Gambardella.

Read More

The series of cartes blanches, published to mark the sixtieth anniversary of the IEE-ULB, continues with an article by Pauline Thinus.

Read More

The series of cartes blanches, published to mark the sixtieth anniversary of the IEE-ULB, continues with an article by Maria Carmela Noviello.

Read More

The series of cartes blanches, published to mark the sixtieth anniversary of the IEE-ULB, continues with an article by Piotr Marczyński.

Read More

The weekly publication of "cartes blanches", scheduled until summer 2024 as part of IEE-ULB's sixtieth anniversary, continues with an article by Martin Deleixhe.

Read More

In 2024, the IEE-ULB turns 60! To celebrate this milestone, its members are invited to reflect on questions about European integration that have been with us since 1964 and that are still relevant in 2024. In a short, accessible format, our researchers draw a mosaic portrait of Europe, between change and continuity.

Read More

The IEE-ULB is thrilled to welcome Theofanis Kakarnias as visiting researcher. Mr. Kakarnias comes to us from Political and Social Sciences department of Pompeu Fabra University in Barcelona, Spain.

Read More

Last September 15, 2023, the IEE authorities welcomed the 60th class of future specialists in EU Studies. It was a moment to dive into the specifics of their programmes and learn about their new academic home and the student associations.

Read More

The IEE-ULB is delighted to welcome Gisela Hernández from the Institute of Public Goods and Policies of the Spanish National Research Council (IPP-CSIC). Her research activities will focus on Rule of Law enforcement in the Council of the EU.

Read More

The IEE is looking for an Executive Manager and Head of Communications for a full-time contractual CDI. All the information about the position and the application process.

Read More

We are thrilled to announce the release of the latest episode of "Making Sense of EU," focusing on the EU, asylum seekers and migrants through the lens of (in)equality. This thought-provoking episode delves into one of the most polarizing topics in EU affairs today – the treatment of asylum seekers in the European Union.

Read More

On Wednesday 31 May 2023, the Institut d'études européennes of the Université libre de Bruxelles (IEE) organised an internal seminar during which PhD, post-doctoral, and visiting researchers had the opportunity to present their on-going work in relation to the protection of the rule of law in the European Union.

Read More

Based on the big success of the two previous years of collaboration with the College of Europe, the third edition of the Debate on the Future of Europe between the IEE and the College of Europe was held on the 20th of June here in Brussels at the Solbosch Campus of the ULB.

Read More

The IEE-ULB is delighted to welcome Chinatsu Yasuda from the University of Tokyo. Her research activities focus on the Cultural Policy of the European Union.

Read More

This is a call for applications for a full-time post-doctoral fellowship for two years (one year renewable once) in European studies and political science, based at the Université libre de Bruxelles (Centre d’étude de la vie politique-CEVIPOL / Institut d'études européennes (IEE)

Read More

Representatives from both our academic and non-academic partner institutions convened in Brussels to present and discuss the progress of their conceptualization of dissensus.

Read More

IEE-ULB visiting researcher Dora Hegedus joins the IEE from LUISS Guido Carli University. Her research activities will focus on the creation of subregions within the EU, and specifically the Visegrad Group.

Read More

The Council of the Institut d'études européennes convened on May 15, 2023 to elect a new leadership team for a two-year mandate (2023-2025) starting on 11 September 2023.

Read More

The one year, full-time, European Communication Officer contract is reneweable. The recruitment process is open until June 7.

Read More

From May 3rd to 5th, the European Union in International Affairs (EUIA) Conference became the place for academics and policymakers to debate the role of the EU in addressing global challenges.

Read More

The IEE-ULB is delighted to welcome Mr. Hein Htet from Sciences Po Bordeaux. His research activities will focus on the evolution of the decision-making process for the steel and financial services in the European Union.

Read More

Why has gender become such a loaded word? As anti-gender campains keep emerging in the EU, we discuss the actors and networks behind them with Professor David Paternotte in our new episode of our podcast Making Sense of EU.

Read More

The IEE-ULB is hiring a post-doctoral fellow to work on "EU instruments and the autocratisation challenge in a dissensus- stricken neighbourhood’ in the framework of the RED-SPINEL Horizon Europe Project.

Read More

The IEE-ULB is looking for a full-time Post-Doctoral Fellow in the framework of Horizon Europe project RED-SPINEL ('Respond to Emerging Dissensus: SuPranational Instruments and Norms of European democracy').

Read More

Dr. Carmen Cristófol Rodríguez from the University of Málaga is our new visiting researcher. Her research activities will focus on Sustainability in the European Fashion Sector. Welcome!

Read More

The IEE-ULB is delighted to welcome Sven Schreurs from the European University Institute. His research activities will focus on the EU social policy from Maastricht to the ‘Next Generation’.

Read More

The IEE-ULB is looking for a full-time research logistician to implement its interdisciplinary research policy.

Read More

The IEE is looking for a full-time Post-Doctoral Fellow in the framework of the Horizon Europe project RED-SPINEL ('Respond to Emerging Dissensus: SuPranational Instruments and Norms of European democracy').

Read More

The authorities of the Institut d’études européennes of the Université libre de Bruxelles and the Faculty of Philosophy and Social Sciences would like to inform you that the tribute ceremony to Professor Mario Telò will be held on Tuesday, March 21st, 2023, at 5 p.m. at the ULB.

Read More

Professor Mario Telò, President Emeritus of the IEE, passed away after a courageous battle with a long illness.

Read More

In early February, the Council held its first ConSIMium in Brussels, a simulation experience for students across Europe. The selected participants played the roles of national negotiators in the Council and European Council. Find out the adventures of the participants Paula and Luisa, two Master's students at the Institut d'études européennes.

Read More

The Institut d'études européennes is delighted to welcome Giuseppe Cannata from Scuola Normale Superiore | Sant’Anna School of Advanced Studies. His research activities will focus on the role of the European Commission in EU policymaking in climate, energy and health policy.

Read More

Making sense of environmental and ecological justice, and the role of the law and of citizen participation in it is not easy. Professors Chiara Armeni & Maria Lee help us understand what's at stake when it comes to decision-making in this area.

Read More

The IEE-ULB is delighted to welcome Katarzina Krzyzanowska from the European University Institute and the Central European University. Her research activities will focus on Constitutional Law, Constitutional Identity and European Values.

Read More

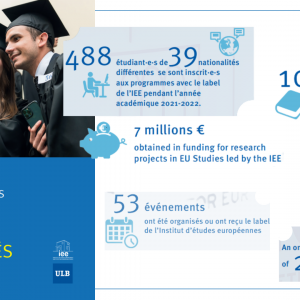

The authorities and members of the IEE look back on a year of collective work which has culminated with the obtention of European funding for several research projects, a deepening of our relations with our privileged partners and with our students and alumni.

Read More

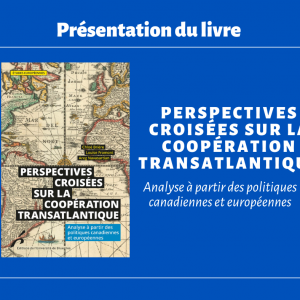

The collective book 'Perspectives croisées sur la coopération transatlantique : Analyse à partir des politiques canadiennes et européennes', edited by Prof. Chloé Brière, Dr. Louise Fromont and Areg Navasartian, affiliated researchers to the IEE was launched on December 5, 2022, at the Institut d'études européennes of the ULB.

Read More

The alumni community of the Institut d’études européennes actively engages with our students and amongst each other through mentoring and networking events.

Read More

War in European soil is the latest test on EU resilience. After living in a polycrisis for the last couple of decades, the European Union is facing one of its toughest trials, one that is pushing it out of its “soft power” approach to international relations. How will the EU handle a return to War in Europe? And how does inequality manifest in this context?

Read More

The Institut d’études européennes is happy to announce the launch of its podcast “Making sense of EU”, a seasonal production that seeks to shed light on EU affairs through the latest scientific research by IEE academics, researchers, and project partners.

Read More

Alicia Hendricks and Raphaele Xenidis win the first edition of the IDEAS-ELJ Best Paper Award and will see their articles published by the European Law Journal after the peer review process.

Read More

The ULB is calling for applications for one full-time doctoral position in the framework of a joint research action (Action de recherché concertée – ARC) around the thematic "Social rights in the European Union (1960-2020): from market to social citizenship and back".

Read More

A second year of rapprochement between IEE and College of Europe students on the future of Europe ended with a day of debate at the Institute.

Read MoreEvery month, in your inbox.